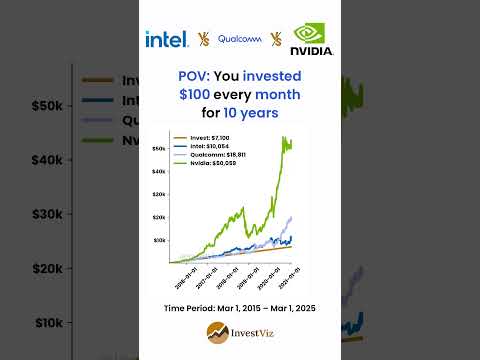

- NVIDIA and Qualcomm, two major players in Silicon Valley, prepare for a potential resurgence following market declines.

- NVIDIA shows promising signs of recovery with a “double bottom” technical pattern and record-breaking earnings driven by AI chip demand.

- Despite positive performance, NVIDIA faces challenges with a high P/E ratio of 38, posing a dilemma for growth-focused investors.

- Qualcomm, offering a low P/E ratio of 16, provides a stable, undervalued option with a strong support line and increased dividends.

- Investors must weigh aggressive growth potential with NVIDIA against Qualcomm’s stability and value.

- Both companies stand ready for change, offering different investment strategies in the volatile semiconductor sector.

Silicon Valley’s two tech titans, NVIDIA and Qualcomm, wait on the precipice of a potential resurgence after recent struggles. Both have journeyed through sharp market declines, leaving investors to ponder the brewing possibilities. As the sheets of silicon dust settle, a remarkable transformation in performance hangs on the horizon.

NVIDIA’s journey resembles a high-stakes drama. The company, once the darling of Wall Street, saw its stock plunge nearly 30% from January highs. Yet, an exquisite technical pattern called a “double bottom” hints at a revival, suggesting that the bullish winds are gathering strength. The company recently shattered records, unveiling an earnings report that exceeded expectations with all-time high revenue. Fueled by insatiable demand for AI chips and data center hardware, NVIDIA’s forward guidance lights a bright path forward.

With analysts like William Blair and Cantor Fitzgerald standing firm in their bullish positions, one might think NVIDIA’s stock would soar unabated. However, the road to recovery remains rocky, shadowed by a lofty price-to-earnings (P/E) ratio of 38. The allure of potentially doubling one’s investment with NVIDIA crashes against the reality of costly shares, creating a bittersweet dilemma for investors drawn to this silicon star.

Quietly preparing its ascent, Qualcomm paints a different picture. Overshadowed by the media blitz surrounding its counterpart, it stands with quiet confidence along a robust support line, refuses to yield to past summer declines. With a remarkably low P/E ratio of 16, Qualcomm presents itself as an enticing, undervalued alternative, especially when compared with industry peers like AMD, whose P/E ratio towers at 114.

Its earnings report told a compelling narrative of its own, surpassing expectations and followed by a dividend increase—a secret handshake of corporate confidence. Qualcomm’s strategy steers clear of headlines, its valuation calling out to risk-averse investors seeking stability in a tumultuous market sea.

So, which titan deserves your trust this quarter? For those with a penchant for aggressive growth and a stomach for volatility, NVIDIA might edge out as the go-to contender. However, value hunters and those with an eye for steady returns may find Qualcomm’s sturdy appeal hard to resist.

Ultimately, the world of semiconductors is unpredictable, but as Q2 opens its curtains, both giants stand poised on the brink of change. Whether you’re a daring risk-taker or a prudent investor, both NVIDIA and Qualcomm offer distinct paths to potential profit. Choose wisely, as each presents a dance of risk and reward in the ongoing saga of the chipmaking industry.

The Battle of Silicon Titans: Why NVIDIA and Qualcomm Are Worth Watching

Industry Forecasts and Emerging Trends

The semiconductor industry is set for significant growth, driven by innovations in AI, IoT, and 5G technologies. According to Gartner, global semiconductor revenue is forecasted to reach $676 billion in 2023, a 13.3% increase from 2022. Both NVIDIA and Qualcomm are expected to play significant roles due to their strategic focus on emerging technologies.

NVIDIA: The High-Risk, High-Reward Contender

How NVIDIA is Leading the AI Charge

– AI Chip Dominance: NVIDIA’s Graphics Processing Units (GPUs) power critical AI applications. With machine learning becoming a backbone of modern applications, demand for high-performance GPUs is skyrocketing.

– Data Center Expansion: The need for massive data processing and real-time analytics is expanding data center capabilities. NVIDIA’s performance in this area has positioned it as a leader in scalable solutions, and companies like Amazon and Google are significant customers.

Speculative Opportunities and Risks

– Valuation Concerns: Despite the promising outlook, concerns about NVIDIA’s high P/E ratio remain (currently at 38), particularly if revenue growth doesn’t sustain at expected levels.

– Stock Volatility: Investors should prepare for potential price swings driven by market sentiment and external economic factors.

Pros and Cons

– Pros: Cutting-edge technology, strong market position in AI and gaming sectors.

– Cons: High valuation, potential regulatory hurdles, and stiff competition.

Qualcomm: The Understated Value Proposition

Low P/E Ratio Advantage

– Competitive Valuation: Qualcomm’s P/E ratio of 16 is considerably lower than its peers, making it an attractive option for value-focused investors.

– 5G Leadership: Qualcomm is a powerhouse in the 5G space, driving advancements in mobile technology and connectivity.

Solid Financial Outlook

– Dividend Increases: Steadily increasing dividends indicate confidence in long-term financial health and are attractive to income-focused investors.

– Resilience to Market Swings: Qualcomm’s diversified product portfolio shields it from extreme market volatility, unlike some competitors.

Pros and Cons

– Pros: Strong 5G position, stable financial track record, reasonable valuation.

– Cons: Lower exposure to high-growth sectors like AI, potential risks from geopolitical tensions, especially around China and supply chain dependencies.

Controversies and Limitations

– NVIDIA: Faces scrutiny over its market dominance and potential antitrust considerations, particularly after its attempted acquisition of ARM.

– Qualcomm: Its reliance on the smartphone market presents a vulnerability, given that significant parts of its revenue depend on handset sales.

Actionable Recommendations

1. Diversify Your Portfolio: Consider balancing investments between high-growth options like NVIDIA and stable performers like Qualcomm to mitigate risk.

2. Monitor Market Indicators: Keep an eye on semiconductor industry trends, regulatory changes, and advancements in AI and 5G technologies.

3. Align with Personal Investment Goals: Match your risk tolerance and investment horizon with the right stock, whether you lean toward aggressive growth or stable returns.

Conclusion

In the face of potential major market shifts, NVIDIA and Qualcomm present unique opportunities for different types of investors. By assessing pros, cons, and market positions, you can make informed decisions that align with your investment strategy.

For more insights on technology and investment trends, visit NVIDIA and Qualcomm.